April 15 is just around the corner although the due date in 2017 is April 18 because the date falls on a Saturday. Even so, people stress over their filing options. While most people will need to file by the deadline, you might have a legitimate reason for filing late.

Reasons for Filing Late

People file their taxes late for many reasons. Some of the most common include.

- Laziness

- Forgetfulness

- Confusion about the filing process

- Medical reason or extended hospital stay

- Poor advice from someone else

- Active military duty or stationed overseas or

- Destroyed records.

Military Exceptions

If you’re in the military, serving in a combat zone, in a hazardous duty area or simply stationed outside the United States, special rules might apply to you. Some of these include additional deductions, extensions, exemptions on some of your pay and more. Check with your accountant for further details.

Submit a Payment with Your Extension Request

You can follow a few simple steps to obtain an extension. The first would be to pay based on what you estimate your taxes to be. Even if you are not sure of the exact amount, by making a decent calculated guess on your taxes and then paying that amount, you can automatically file for an extension. Once you actually file your taxes, you can pay the difference to the Internal Revenue Service or request a refund for what you over payed. This is the best method available for someone who does not have their taxes deducted from their paycheck, such as subcontractors or restaurant servers. On the other hand, if you do have your taxes deducted from your paycheck and suspect that you are owed money, then you have already completed this step.

Use the Correct Forms

However, you must realize that an extension does not change the fact that you still have to pay your taxes by April 18. Once people determine what point they are at the above steps, they can proceed to file for an extension. This allows you to extend your filing deadline for six whole months until October 16 and is available to anyone for any reason. You have three ways to obtain an extension.

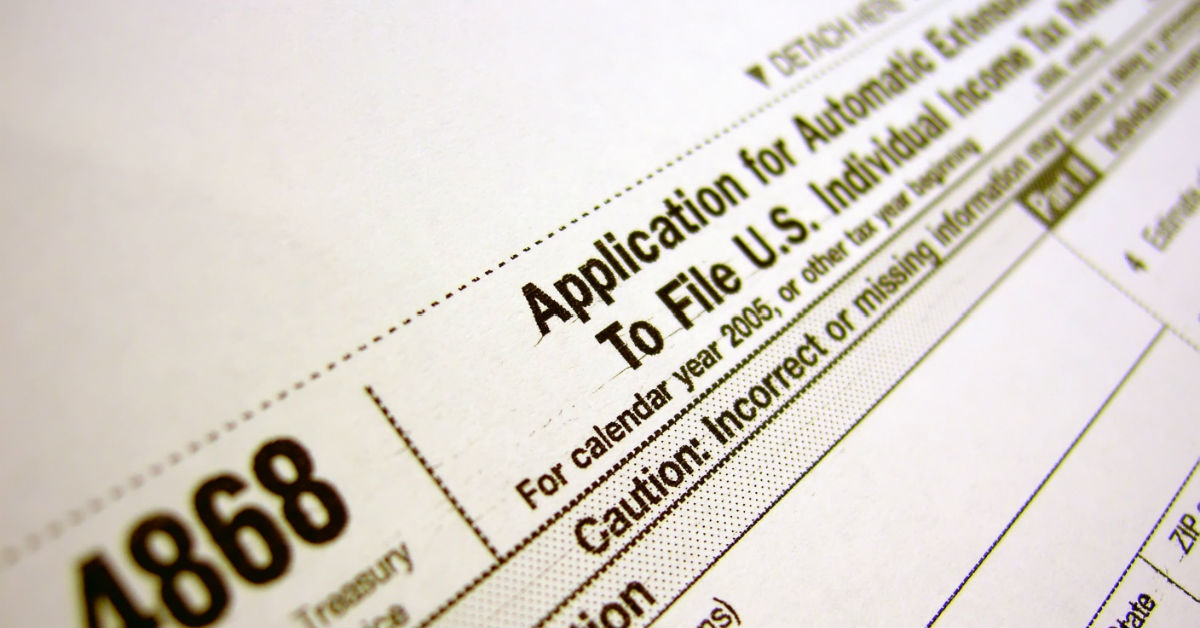

- File Tax Form 4868 online.

- File Tax Form 4868 by mail.

- Use your credit card or debt card via the Electronic Federal Tax Payment System (EFTPS) to pay at least part of your income tax due. You should pay what you expect to owe.

Remember to read the instructions carefully for Tax Form 4868 before filing and make sure you understand all of the details. If you miss the filing date and if you owe taxes, you will accrue hefty late fees. However, as long as you make a payment, you can avoid these fees.

If you are stressed about paying late or if you feel confused about the process, you can simply find help from a reputable tax and accounting service that charge reasonable rates. The fee that you pay them will likely be far more reasonable than any penalty the IRS might impose for failing to file your taxes on time.